Shop Now, Pay Later: Loan Apps That Work Like Affirm App Development

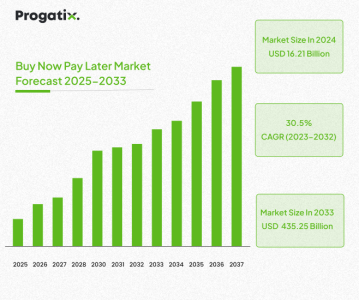

Flexible Buy Now, Pay Later (BNPL) options are in demand across shoppers globally. These platforms enable customers to split payments into smaller ones, allowing them to get the goods now and pay for them later. According to straitreserach’s report, the global buy now pay later market size was estimated at USD 39.65 billion in 2024 and is anticipated to reach from USD 51.74 billion in 2025 to USD 435.25 billion by 2033, increasing at a CAGR of 30.5% during the forecast period.

Apps like Affirm have formed strong partnerships with major retailers, positioning themselves as key players in the buy now, pay later (BNPL) space. In this blog post, we’ll explore Affirm and its top alternatives, diving into their features, benefits, and drawbacks to help you find the best loan app for your needs. Let’s dive in!

What is an Affirm App?

Affirm is a leading financial technology app used in the point-of-sale lending industry, established back in 2012 in San Francisco, delivering consumers a simple, adaptable, and visible way to finance purchases. It is one of the leading Buy Now, Pay Later (BNPL) solutions in the USA, offering shoppers a BNPL service that lets them divide their purchases into smaller, fixed payments over a set period, usually for a week to several months.

The Affirm platform has a 40 million customer base since its introduction and engages with more than 245k merchants. Affirm offers short-term loans at checkout and enables the terms of these loans to vary by merchant. Repayment plans involve 3 to 6 months, and a 12 12-month option. There are two ways of payment offered by Affirm:

- 4 interest-free payments every 2 weeks;

- Monthly installments.

For instance, on a $500 purchase, you could pay $125 every 2 weeks without APR (Annual Percentage Rate) or select monthly payments for 3/6/12 months at 0-36% interest.

Affirm charges no late, prepayment, annual, or account opening/closing fees. The standard limit for all Affirm services is $30,000.

Additionally, users could manage their accounts via the Affirm app or online and set up AutoPay to ensure timely payments. The app is available on iOS, Android, and as a Google Chrome extension for the web.

Pros of Affirm

- No late, payment, annual, or account opening/closing fees.

- A virtual card feature for receiving a one-time credit card number that expires in 24 hours.

- Flexible payment options, with monthly payments beginning from 3 months.

- Collaborate with a few of the most renowned brands and stores.

- Offers BNPL as well as POS loans.

- No interest when paid in 4.

Cons of Affirm

- High interest rates up to 36%.

- Unable to reschedule payments.

- Limited choice of merchants.

- May or may not offer a high spending limit.

Features

- Electronic payments: Allow payments via ACH or bank transfer.

- Self-service portal: Lets users manage payments and accounts individually.

- Transaction monitoring: Tracks transactions for problems or irregularities.

- Payment fraud prevention: Guards against fraud during transactions.

- Debit/Credit card processing: Enable payments through debit or credit cards.

- Order tracking: Tracks the status and shipping of purchases.

- Activity dashboard: View transactions, payments, and account activity.

- Credit card processing: Accepts credit card payments.

- Real-Time data: Offers live updates on transactions and account info.

- Reporting & statistics: Shows insights into spending and payment history.

Apps Similar to Affirm

Let’s review the best apps like Affirm.

-

AFTERPAY

App Store: 4.9

Play Market: 3.8

Website: https://www.afterpay.com/

Afterpay is one of the top buy now, pay later (BNPL) providers globally and a strong competitor to Affirm. Like Affirm, the company provides installment loans that enable consumers to buy goods and services now and pay for them over time. Its business model centers on offering consumers an interest-free alternative to credit cards, while offering interest-free payments in 4 installments and 6 and 12-month plans on a monthly basis.

Afterpay loans break down your purchase into four equal installments, each due every 2 weeks. The service automatically deducts every installment amount from your selected payment method on the scheduled due date.

You could make payments any time before your due date. This system allows you to manage your balance quickly and free up your credit limit for upcoming purchases. You could choose one of the selected Afterpay payment methods for automatic deductions, including a debit card or a bank account.

Afterpay charges no interest on your purchases as long as you make all the payments on time. Missing Afterpay payments incur late fees of up to 25% of the order.

Pros

- Like Splitit, Afterpay offers BNPL loans.

- No interest required.

- There is no credit check.

- Doesn’t impact your credit score, just helps set your spending limit.

- Payments are split over 6 weeks with four installments.

- Manage payments and shop through the well-rated app.

- Available at thousands of retailers.

Cons

- Requires a down payment, like Zebit.

- Late fees apply for missed payments, varying by state.

- Orders may be declined based on financial eligibility.

- The initial spending limit is around $600.

Key Features

- Interest-Free: Split payments into four installments over 6 weeks, no interest if paid on time.

- Flexible Payments: Payments are every 2 weeks, and you can adjust your schedule or choose a preferred day.

- Pay Early: Pay off your balance early with no fees.

- Reschedule: Change payment dates (except the first and last) by contacting support.

- App: Easily manage payments and shop through the app.

- Afterpay Card: Use a digital card in Apple/Google Wallet for contactless in-store payments.

-

SEZZLE

App Store: 4.9

Play Market: 4.6

Website: https://sezzle.com/

Sezzle, one of Affirm-like apps, is a quickly growing BNPL platform that offers an adaptable way to manage purchases by enabling consumers to split their purchases into interest-free installments. Its model centers around delivering a “Shop Now, Pay Later” experience, providing users more control over their finances. When purchasing through Sezzle, customers could spread their cost into four equal installments, paid over 6 weeks.

Sezzle is a preferred option for those cautious regarding their credit history. Integrating with several online retailers allows for a streamlined and effective checkout experience. Once a purchase is made, Sezzle automatically deducts the installments from the user’s connected debit or credit card, simplifying the repayment process.

Pros

- Pay over 6 weeks with no extra cost.

- Available at 30,000+ stores, including major retailers.

- Choose from 4 payments over 6 weeks, two payments over 2 weeks, or monthly plans with reasonable interest rates.

- It won’t impact your credit score.

- Simple and straightforward payment plan structure.

Cons

- A late fee is charged for a missed payment.

- Missing payments can negatively affect your credit score.

- Monthly plans carry interest rates between 5.99% and 34.99%.

- Requires 25% of the order paid upfront.

Key Features

- Interest-free installments: Split payments into four installments over 6 weeks without interest if paid on time.

- Financial wellness tools: Manage payments and track financial health.

- Payment rescheduling: Reschedule payments with certain limits.

- Spending limits and tracking: Set spending limits and track payments.

- Merchant integrations: Available at 30,000+ retailers like Target and Nike.

Get a Scalable Sezzle Clone App Built

Let's Connect

-

ZIP

App Store: 4.9

Play Market: 4.8

Website: https://zip.co/us

Zip, formerly known as Quadpay, is one of the key players in the buy now, pay later industry, like Affirm, offering a simple and easy BNPL plan and partnering with a huge number of merchants. It enables consumers to split their purchases into four equal payments over six weeks, making budget management easier without additional cost.

Available to everyone, Zip does not require a credit check. It could be used through any credit or debit card at thousands of stores, both in-store and online. Whether you are buying clothes, electronics, or everyday items, Zip helps you expand payments and makes shopping more convenient.

Pros

- Zip Pay offers interest-free installments.

- Multiple plans for different needs (Zip Pay, Zip Money, Zip Business).

- Simple and straightforward payment system.

- Popular and widely accepted locally.

- Only small fees for missed payments.

Cons

- Lacks features like credit building and longer terms offered by competitors.

- Limited global reach and more established in Australia.

- Offers shorter-term repayment periods.

Key Features

- Interest-free payments: Split purchases into interest-free installments with Zip Pay.

- Instant approval: Quick approval for purchases with Zip.

- In-store and online use: Use Zip for both online shopping and in-store purchases.

- Spending tracking: Manage payments and track spending through the app.

- Merchant network: Shop at many partner merchants accepting Zip.

-

VIABILL

App Store: 4.9

Play Market: 3.4

Website: https://viabill.com/us/

ViaBill is a rapidly growing fintech company offering flexible payment options to consumers. It provides two main payment plans: Standard and ViaBill+, and integrates smoothly with various e-commerce platforms. Competing with Affirm for market share, ViaBill stands out with its interest-free installment plans and no credit checks, making it accessible to a wide range of customers.

ViaBill is mainly appealing to those who value transparency in financing, offering clear terms before any commitment. Emphasizing smaller purchases makes it a great option for everyday shopping requirements, unlike Affirm, which tends to center on larger-ticket items with extensive repayment periods.

Accepted by numerous in-store and online retailers, ViaBill is used across categories like fashion, electronics, beauty, home goods, and travel. Big-name retailers such as Expedia, Walmart, Amazon, Kmart, AliExpress, Zazzle, Puma, and Rakuten are just a few that support ViaBill.

Pros

- Interest-free payments.

- Offers several flexible installment options.

- Accessible without credit checks.

- Widely available to many top retailers.

- Low setup fee for a higher limit.

Cons

- High late fees for missed payments.

- Limited standard plan, available only for selected stores.

- A setup fee is needed to activate.

- The Standard plan has a 1-year limit.

Key Features

- Interest-free installments: Split purchases into interest-free payments.

- Flexible Payment Options: Offers Standard and a ViaBill+ plan.

- Flexible Payments: You can choose 4–24 installments with ViaBill+.

- In-store & Online: Use to contribute to online and in-store retailers.

- No Credit Checks: No credit check needed for approval.

- Extensive Merchant Network: Recognized at huge retailers like Amazon, Walmart, Rakuten, Puma, and many more.

-

SPLITIT

App Store: 4.8

Play Market: 4.6

Website: https://www.splitit.com/us/

Similar to Affirm and Klarna, Splitit is an exceptional Buy Now, Pay Later lender. However, unlike traditional BNPL services, Splitit leverages your existing credit card for the installment process, which eliminates the need for additional credit checks or new financing applications. The service works by placing a hold on your credit card for the total purchase amount, which is then reduced with each installment payment.

With Splitit, there’s no interest or fees as long as payments are cleared on time, and there’s no minimum credit score needed to use the service. This makes it a striking option for those who want to spread out their payments without the difficulty of applying for new credit. Splitit also stands out by offering the flexibility to split purchases into up to 24 equal payments, giving users more time and control over how they pay.

Pros

- Similar to AfterPay, it offers BNP loans.

- No credit check required.

- No interest fee needed.

- Allows you to keep earning credit card rewards.

- No prepayment or late payment fees.

Cons

- Not all credit cards work.

- A credit card is required to use Splitit, such as an American Express.

Key Features

- No New Credit Applications: Use your existing credit card for installments.

- Interest-Free Payments: Split payments with no interest if paid on time.

- Flexible Payment Terms: Choose from up to 24 equal payments.

- Installment Builder: Tailor the number of payments, amounts, and due dates.

- Wide Credit Card Acceptance: Supports Discover, UnionPay, Visa, and Mastercard.

- No Minimum Credit Score: Available for everyone, irrespective of credit score.

- Retailer Partnerships: Available at platforms like GlassesUSA, REST, James Allen, and Echelon Fitness.

Start Developing a Splitit Inspired App Now

Let's Connect-

KLARNA

App Store: 4.8

Play Market: 4.6

Website: https://www.klarna.com/

Klarna is one of the leading buy now, pay later (BNPL) services, offering a flexible way to shop and pay over time. Similar to Affirm, Klarna enables users to divide their purchases into manageable payments, with no minimum credit score needed to get started.

With more than 150 million users and partnerships with 500,000+ merchants, Klarna gives you access to wide-ranging popular brands, including Nike, Sephora, Wayfair, Harley-Davidson, MLBShop.com, and NHLShop.com.

Klarna offers numerous payment options: the interest-free “Pay in 4” plan, where your purchase is split into four equal installments; “Pay in 30 days,” which gives you additional time to pay with no interest; and a simple “Pay now” option for those who choose to pay upfront. For larger purchases, you can also choose monthly financing plans ranging from 6 to 24 months.

There’s a $10 minimum for all transactions, but new users receive a $5 bonus after making their initial purchase, a nice little bonus for getting started.

Pros

- Like Affirm, Klarna offers POS and BNPL loans.

- No credit check required.

- It collaborates with a few of the most well-known brands and stores.

- No interest is required when paid in 4.

- No prepayment or late payment fees are needed.

Cons

- No applications are approved.

- Klarna might or might not offer a high spending limit.

Key Features

- Pay in 4 Installments: Split your purchases into four equal, interest-free payments.

- Interest-Free Financing Options: Enjoy flexible payment plans with no additional cost when paid on time.

- Mobile App with Purchase Tracking: Allow easy management and tracking of your purchases directly via the app.

- Merchant Partner Network: Shop with a wide range of popular brands and retailers that collaborate with Klarna.

- Soft Credit Checks: Accomplishes a soft credit inquiry, which won’t influence your credit score.

-

PAYPAL CREDIT

App Store: 4.8

Play Market: 4.3

Website: https://www.paypal.com/ca/home

PayPal Credit makes it easy to shop now and pay later, all within the PayPal platform you probably already use. It offers adaptable options like “Pay in 4” interest-free installments, or longer-term financing for bigger purchases, with quick credit decisions at checkout. Since it’s built right into your PayPal account, there’s no requirement to sign up for an individual service or download a new app. And more, because PayPal is recognized by so many online stores, you don’t have to worry about whether a retailer supports it; it just works.

Like Affirm, PayPal Credit gives you more control over how and when you pay, but with the additional bonus of being nearly universal. It’s ideal for anyone who already uses PayPal and wants simple financing without the difficulty. Everything is in one place, from your payment options to your transaction history, making it easy to stay on top of your expenditure.

Pros

- Integrated directly into your PayPal account, no additional sign-up or app required.

- Offers both short-term and comprehensive payment plans to suit different budgets.

- No yearly charge to use the service, unlike traditional credit cards.

- Widely accepted across millions of online stores.

Cons

- Extended financing plans can come with steep interest if not paid fully.

- Late or missed payments can be reported and affect your credit score.

- You may be charged extra fees if you miss a payment deadline.

Key Features

- Pay in 4 Installments: Split your purchase into four equal payments, without interest or fees.

- Extended Payment Plans: Choose flexible repayment options over several months.

- No Interest if Paid in Full: Avoid interest charges as long as the full balance is paid on time.

- Universal Merchant Acceptance: Use Klarna at thousands of retailers, both online and in-store, across various industries.

- Integrated with PayPal Wallet: Easily link and pay using your PayPal wallet when shopping with Klarna.

Start Developing Your PayPal Credit Alternative

Let's Connect-

UPLIFT

App Store: 4.7

Play Market: 4.1

Website: https://www.uplift.com/

Uplift is a leading buy now, pay later (BNPL) platform built specifically for travel. Whether you’re booking flights, hotels, cruises, or full vacation packages, Uplift allows you to split the cost into fixed monthly payments. The application process is fast, with quick loan decisions based on your credit profile, and repayment terms could extend up to 24 months. Unlike many other BNPL providers, Uplift doesn’t charge late fees or prepayment penalties, although interest rates can range from 0% to 36% based on your creditworthiness.

What sets Uplift apart from competitors such as Affirm is its exclusive emphasis on the travel industry. The platform partners right away with major airlines, hotel chains, and travel agencies, including brands such as Air Canada, American Airlines, and Atlantis, to integrate its payment option at checkout. This makes it effortless for travelers to budget and book trips without having to pay the complete cost upfront. Available in both the U.S. and Canada, Uplift is perfect for anyone looking to finance travel in a simple and adaptable way.

Pros

- Fixed monthly payments, ensuring easier budgeting.

- Easy to qualify for, making travel financing accessible to more people.

- Works with a wide range of airlines and hotels for easy booking.

- Personalized exclusively for booking trips, with partnerships across key airlines and hotels.

- More forgiving terms compared to some general BNPL services.

- Helps travelers plan and manage their travel budgets more effortlessly.

Cons

- Missing payments can result in extra charges.

- Interest rates could be higher compared to traditional loans.

- Some financing options might include fees as per the plan.

Key Features

- Travel-Specific Financing: Designed specifically to help you finance trips, including flights, hotels, and vacation packages.

- Transparent Payment Terms: Clear, upfront pricing with no hidden fees or surprises.

- Quick Application Process: Quick decision-making within seconds during checkout without lengthy forms.

- Airline and Hotel Partnerships: Works directly with key travel brands for smooth booking and payment.

- Flexible Payment Schedules: Choose from numerous installment plans that fit your travel budget.

-

PERPAY

App Store: 4.6

Play Market: 3.8

Website: https://perpay.com/

PerPay is a buy now, pay later (BNPL) platform that combines interest-free shopping with an emphasis on helping users build or repair their credit. Unlike traditional BNPL services, PerPay requires users to connect their direct deposit, and payments are automatically withheld from their paycheck. The service offers flexible repayment terms of up to six months, excluding interest charges or late fees. However, items don’t ship until your first payment is received, which means you’ll need to wait until payday if funds aren’t yet accessible. Purchases are made via PerPay’s exclusive marketplace, featuring over 1,000 top brands such as Apple, Samsung, and Michael Kors.

One standout feature is PerPay+, an optional credit builder program that reports on-time payments to the major credit bureaus, Experian, Equifax, and TransUnion, making PerPay a great option for users who want to enhance their credit while shopping reliably. As per the PerPay, users in the credit-building program have seen an average score increase of 39 points. With no interest, no hidden fees, and a user-friendly repayment structure, PerPay is specifically appealing to those with unreliable credit or restricted access to traditional financing.

Pros

- Similar to Splitit, Perpay offers BNPL loans.

- No interest or no additional fees required.

- Using the app could help rebuild your credit.

- No credit check needed.

Cons

- Not all applicants get approval.

- No item gets shipped until Perpay gets its first payment.

Key Features

- Interest-Free Payments: Repay purchases over time without paying interest.

- Automatic Deductions: Payments are taken directly from your connected paycheck.

- Exclusive Marketplace: Shop from 1,000+ popular brands within PerPay’s platform.

- Flexible Terms: Select repayment plans ranging from one to six months.

- Credit Building with PerPay+: Option to report payments to credit bureaus, improving your score.

- No Late Fees: Missed payments won’t incur penalties, offering a stress-free experience.

-

ZEBIT

App Store: 3.1

Play Market: 3.2

Website: https://preview.zebit.com/

Zebit, one of the best loan apps like Affirm, aims to help individuals with restricted credit options, offering a buy-now-pay-later service. It allows consumers to buy numerous products, from electronics and home goods to fashion. You could pay for more than six months, with no hidden fees. The payment plans are adaptable, not impacting your credit score across the application process.

Though there are some key considerations to remember before using Zebit, firstly, products on Zebit might be more costly than those found elsewhere. Secondly, you will need demonstrable income to qualify for credit via Zebit. Also, Zebit does not report payment history to credit bureaus, so it would not help build your credit score. Lastly, unlike many retailers, Zebit does not offer refunds or returns for surplus items.

Pros

- No fees or interest needed.

- Amounts ranging from $1000 to $2,500 can be borrowed.

- Approval doesn’t depend on your credit score or history.

- Like Splitit, Zebit offers BNPL loans.

- Built-in marketplace within the app to shop and finance products.

- Prioritizes everyday items like electronics, home, and personal care.

- Get approved quickly without extended applications.

Cons

- Management fee for gift card purchases.

- Similar to Afterpay, you are required to put money down.

- Residents of Washington, D.C., cannot apply.

- Products in Zebit’s catalog are normally overpriced.

- Shipping could be slower than at other retailers.

Key Features

- Interest-free financing: Pay for purchases over time with no interest.

- Up to $2,500 credit limit: Access a spending limit of up to $2,500 for approved users.

- Integrated marketplace: Shop directly within a built-in platform offering numerous products.

- Essential goods focus: Prioritizes access to daily necessities like groceries and household items.

- No traditional credit checks: Approval doesn’t rely on standard credit scores or reports.

- Web and mobile access: Use Zebit easily on desktop or mobile browsers.

Final Views: Find the BNPL App That Works for You!

Buy Now, Pay Later (BNPL) apps like Affirm have reformed retail financing by providing flexible, interest-free payment options. Whether you’re shopping for basics, fashion, or travel, there’s a platform that fits your lifestyle.

Every app serves a niche:

- Klarna controls fashion retail.

- Splitit uses your existing credit card.

- Uplift emphasizes travel bookings.

- Zebit helps users with restricted credit access essentials.

- PayPal Credit is widely recognized.

Selecting the right BNPL app relies on your shopping habits, payment adaptability needs, and whether you want features such as credit building or broad merchant support.

As BNPL services grow, they offer a smart substitute to traditional credit, assisting you in staying on budget with no interest or fee payment.

Why Choose Progatix?

Looking to build a BNPL app like Affirm or enhance your existing platform? Progatix can help change your vision into a reality. With extensive experience in custom software development, we skillfully create smart, user-friendly fintech solutions that scale with your business. Whether it’s a mobile app, a web-based platform, or an all-in-one SaaS product, our team works thoroughly with you to design and develop tools that are safe, flexible, and easy to use. We’ve earned the reliance of global brands by delivering outcomes that truly make a difference, and we’re ready to do the same for you.

Turn Your BNPL App Idea Into Reality

Let's Connect

Let's Discuss Your Tech Solutions

Let's Discuss Your Tech Solutions